The Financial Garden Analogy

Imagine your financial life as a garden. Most people are busy watering the lawn (their regular job) because that’s what everyone around them is doing. The green grass looks nice, but it needs tending every month. If you stop, it quickly dries up.

Realized the real lesson from "Rich Dad Poor Dad" isn’t just about planting one big tree (like buying real estate). It’s about knowing the difference between plants that keep giving back year after year—your fruit trees (assets)—and weeds that soak up water but never bear fruit—liabilities.

Your goal isn’t just to have the biggest patch of green; it’s to plant things that feed you, provide shade, and maybe even give you something to trade with neighbors. You learn to spot which seeds to plant (financial literacy), make sure you always set aside some water for the important stuff first (pay yourself first), and over time, your little garden starts to produce more on its own—even when you’re not tending it all day.

If you only focus on what everyone else is doing, you might end up with a high-maintenance yard that looks good but wears you out. But if you think about what you want, choose your plants wisely, and learn a little about gardening along the way, you end up with a place that takes care of you—and maybe even frees up your afternoons to help neighbors start their own.

Enjoy the episode!

YouTube & The Episode Hub

Available on:Apple Podcasts •Spotify •Overcast •Pocket Casts •Castbox •YouTube Music •Amazon Music •Audible •Substack • Everywhere you canlisten

Highlights From The Episode:

- Assets vs Liabilities: The biggest eye-opener is super simple: assets put money in your pocket, liabilities take it out. Most people accidentally collect liabilities—think new cars, gadgets, or even that house you live in—but the wealthy stack up assets that actually pay them.

- Financial Literacy Matters: It’s not about how much you make—it’s about how much you keep and how you manage it. Learning basic financial concepts gave Speaker A real confidence. Don’t be intimidated by big terms—just start learning and asking questions when you don’t know something.

- Pay Yourself First: When you get paid, put something (no matter how small) aside for yourself first before bills and fun. Build the habit now, not “once you have more.”

- Look for Opportunities: Start shifting your mindset from “I can’t afford this” to “How can I afford this?” It’s amazing how your brain begins to spot chances when you give it a job.

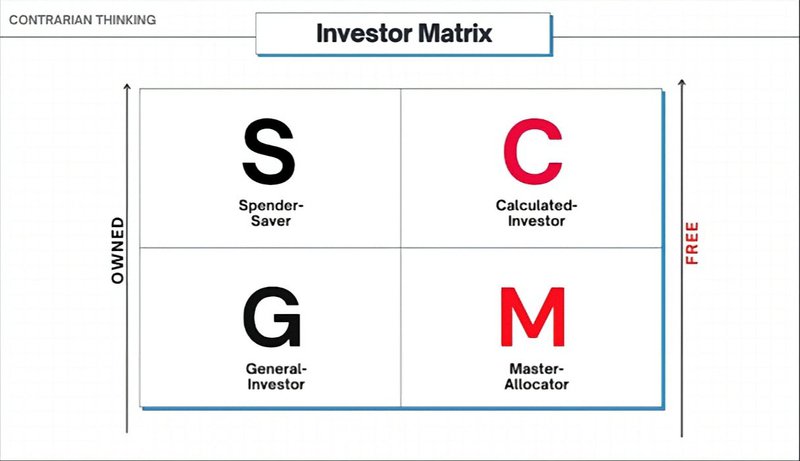

- Test Your Approach: Try the Cashflow board game (there’s even a digital version). Speaker A found it revealed his real investing style—and it’s a low-stakes way to practice decisions.

- Be Careful With Debt: Good debt helps you buy assets that pay for themselves. Bad debt (like credit cards for shopping sprees) just drains you. If you’re going to leverage debt, know your plan and start small.

- Choose Your Mentors and Advisors: Pay for good advice from people with real experience (and skin in the game). Don’t fall for every seminar or online “guru.”

- Make Conscious Choices: The real theme of this episode—don’t just drift along on autopilot or do what everyone else says you “should.” Decide what YOU want your work, finances, and life to look like. Get your spouse or partner on board. Then take a real, small step in that direction.

“Most people spend their entire lives working for money instead of building systems that make money for them.” Tyson Gaylord. It’s easy to follow advice without ever asking if it fits your real life. My story is a reminder to check the source, challenge assumptions, and choose the path that matches your values and goals.

Your biggest asset? The willingness to think for yourself.

✨ Legendary Weekly Challenge ✨

Take intentional steps toward shaping the life they want.

Here’s what to do:

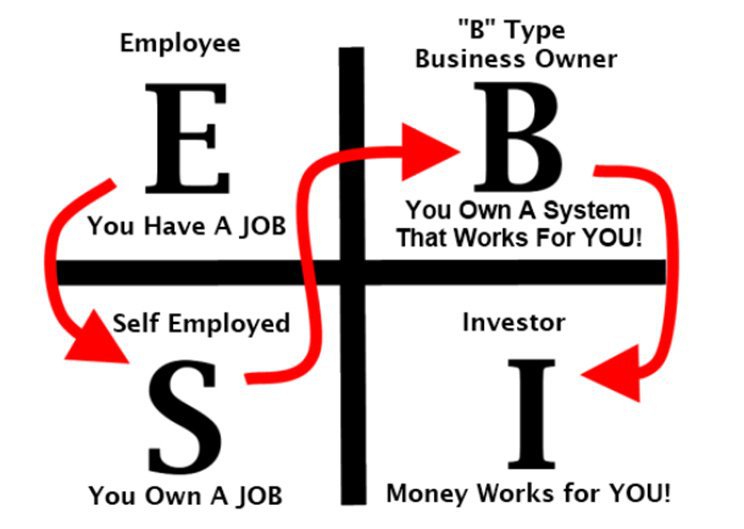

- Sit down and list out how you want your life to look.

Think about the type of employment you want, do you want to stay an employee (E), maybe move over to self-employed (S), or dabble in business ownership (B) and investing (I), or a combination? Decide what fits you best. - If you have a spouse or partner, talk about your plans together.

Each person should share their own goals, then find ways to align and create a joint plan for your family or partnership. - Take one small action right away.

This could be putting a reminder on your calendar, making a phone call, opening an account, ordering a relevant book, whatever moves you closer to your goal. - Every day, commit to one step forward.

Keep the momentum by taking daily action, even if it’s small.

The goal is to move from planning to doing, so you’re actively creating the future you want.

Meet Robert Kiyosaki

Robert Kiyosaki is a polarizing entrepreneur and investor who challenged conventional financial wisdom by introducing the Cashflow Quadrant. In the book, he contrasts his highly educated father's traditional advice with the street-smart business acumen of his best friend's entrepreneurial father. The narrative shows how the wealthy systematically acquire income-producing assets while the middle class unknowingly accumulates liabilities. Kiyosaki used this philosophical shift to build a global education empire, yet his tactical advice often draws criticism from financial professionals for being simplistic, speculative, and sometimes legally risky.

Visit Rich Dad

Rich Dad Poor Dad uses the conflicting financial advice of two father figures to spark a radical cognitive shift regarding personal wealth. The fundamental lesson is that readers must understand the strict mathematical distinction between an asset, which puts money into your pocket, and a liability, which takes money out of your pocket. Ultimately, the book argues that the middle class remains trapped in a cycle of paycheck dependency because they unknowingly purchase liabilities, whereas the wealthy adapt and achieve total autonomy by systematically building businesses and acquiring assets that generate passive income.

SELECTED LINKS FROM THE EPISODE

Visit RichDad.com for books, the game, and more resources for your financial education.

Rich Dad Classics Boxed Set

CASHFLOW Board Game

CASHFLOW Board Game Online Edition

Rich Dad Media Network Podcasts

Cashflow Quadrant

Two episodes we did, breaking down the Cashflow Quadrant's

Cashflow Quadrants PT 1 | EP 9Tyson Gaylord

CashFlow Quadrants Pt. 2 | Ep 10Tyson Gaylord

Rich Dad Poor Dad Lied To You by Codie Sanchez

- Jasmine DiLucci | Tax Attorney, CPA, EA

MONEY Master the Game: 7 Simple Steps to Financial Freedom (Tony Robbins Financial Freedom Series)

Failing Forward: Turning Mistakes into Stepping Stones for Success

Connect With Us

Facebook | Instagram | Twitter | YouTube| LinkedIn

More Podcast Apps: TheSocialChameleon.Show/Podcast-Show

#SocialChameleonShow #RichDadPoorDad #RobertKiyosaki #FinancialLiteracy #PassiveIncome #PersonalFinance #WealthBuilding #MindsetShift #CashflowQuadrant #InvestingTips #MoneyMatters #FinancialFreedom #SocialChameleonShow #BookReview #AssetVsLiability #LevelUpYourFinances #FinancialEducation #MoneyMindset #FinancialGrowth #SmartInvesting

Show notes and transcripts powered with the help of Castmagic.

Comments

Post a Comment